Payback is a simple and easy calculation but inadequate by itself. By Jeff Ross November 15, 2013 Supplychain247.com

Capital budgeting—planning for the acquisition of long-lived assets—is serious business.

Capital investments have a major financial and operational impact, often determining scalability and operating efficiencies for years to come. As a result, these investment decisions are critical if the organization is to achieve its long-term profitability goals.

In many organizations, including those with DC operations, it is common to initially evaluate a capital project in terms of the payback period.

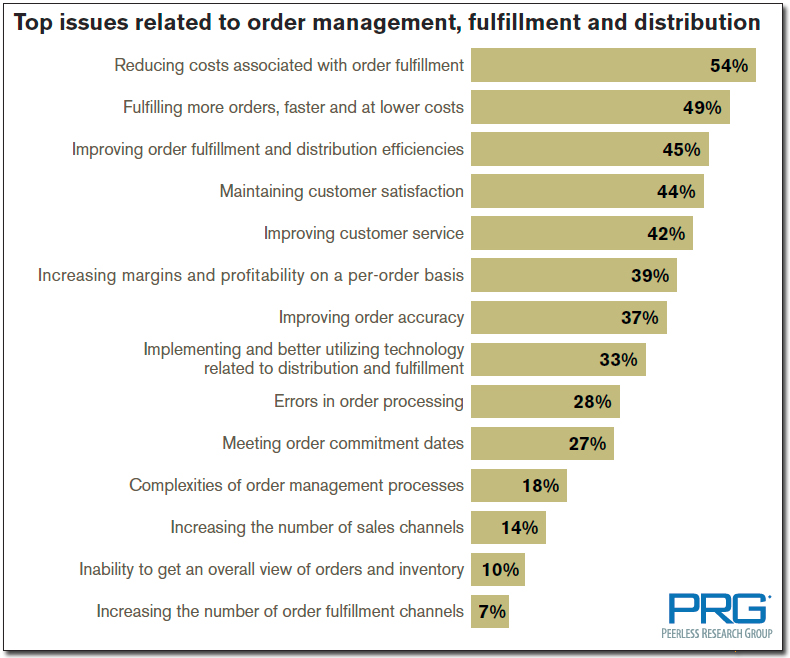

A recent Peerless Research Group poll of DC executives revealed that 27% of respondents expected a ROI in 6-to-12 months while 36% anticipated a 12-to-24 month payback.

As a stand-alone method, payback is simple to calculate and easy to understand-an absolutely perfect tool for those of us challenged by the mathematical machinations of anything beyond addition and subtraction much less the inclusion of multiple variables. But payback has serious limitations as it does not account for the time value of money, risk factors, financing rates, depreciation schedules, opportunity costs or other important considerations.

When asked to invest millions of dollars in DC automation, senior managers will not be comforted by a quick payback alone. They’ll demand a more sophisticated analysis with more credible projections as to the investment’s total payoff throughout the years.

Most CEOs, CFOs and COOs rely upon discounted cash flow techniques (DCF) to get a better handle on the downstream impact of their capital investment decisions. The two most widely applied DCF methods are net present value (NPV) and internal rate of return (IRR). When used in conjunction with the payback method, DCF techniques have the potential to powerfully influence the decision to move a capital project forward.

With these methods, the expected cash flows of a potential investment are discounted to their present values using the company’s minimum desired rate of return. The sum of the value of all cash flows, including the incremental investment, determines the desirability of the project. If the sum is positive-meaning the present value of cash inflows exceeds the present value of cash outflows-then the investment promises a time-adjusted rate of return higher than the company’s minimum accepted rate of return. Said another way:

- NPV is the present value of future returns, discounted at the cost of capital, minus the cost of the investment.

- IRR is the interest rate that equates the present value of future returns to the investment outlay.

This is not an easy concept for us non-financial types to grasp, but this is the context within which your management team will decide the fate of your proposed DC automation project.

And this is precisely why in the previous blog we recommended recruiting a competent financial analyst to your project team.

So here’s the summary:

- You’re convinced warehouse automation will be immensely favorable to the company’s bottom line and its long-term competitiveness/success.

- With an informed guesstimate of the DC upgrade cost, you’ve fixed the length of the expected payback or ROI.

- Your argument has been buttressed with professional-grade DCF analysis.